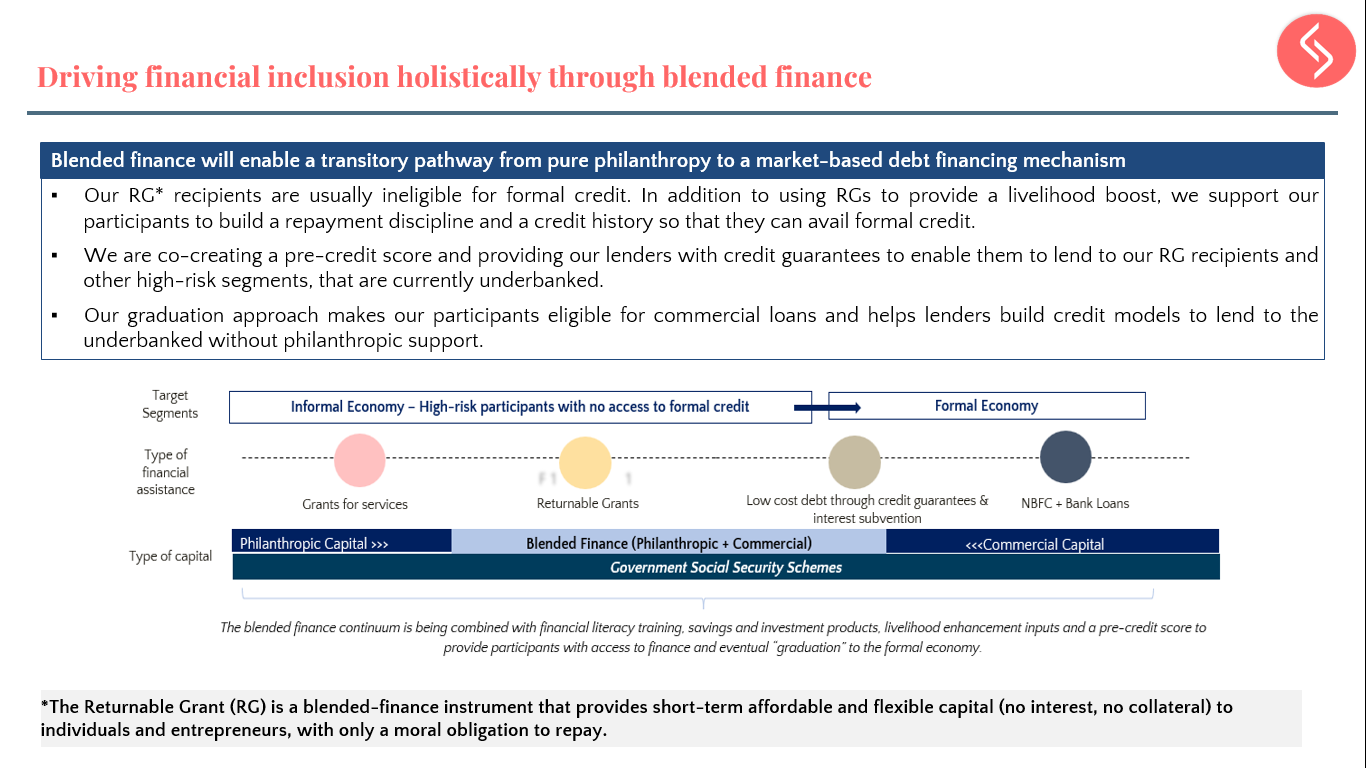

Ever since COVID-19 hit India, the disease brought an onslaught of unimagined and unprecedented circumstances. Governments scrambled to impose lockdowns on short notice to control the spread of the disease and India was no stranger to adopting this global approach to control the infections. However, this strategy came with a set of complex implications that bore an impact on health, livelihoods, education and life as we “normally” knew it.

The COVID-19 crisis has evidently affected livelihoods and brought income shocks to the working classes. This shock has been accompanied by an unanticipated shift to the digital mode and accelerated digitization in the country. To understand the impact of COVID-19 on India’s digital appetite, KPMG conducted a survey and illustrated its findings as following:

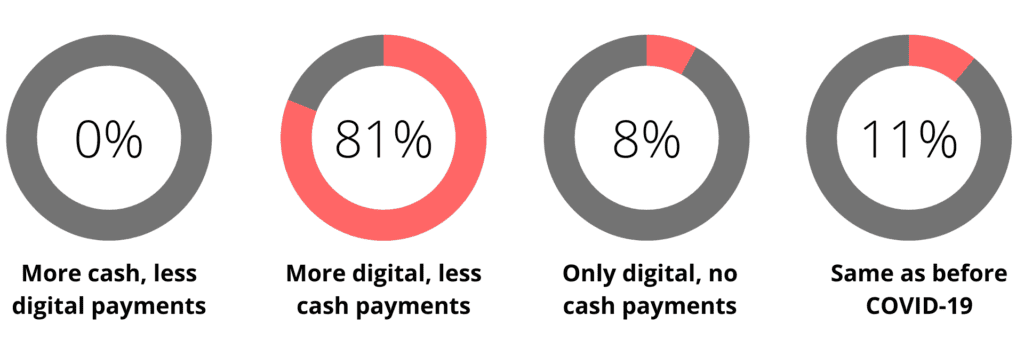

What is the impact of COVID-19 on the usage of digital payments?

As the survey demonstrates, 81% of the respondents claimed a higher usage of digital payments as compared to cash in 2020. Whereas none of the respondents reported a higher usage of cash over digital payments.

The restrictions that were brought about as a result of COVID-19 not only hampered mobility, but also fostered a sense of fear among the common public. While white-collar workers were able to fall back on business-enabling tech platforms that they were already using, the livelihood of blue-collar workers and small business owners who carry out much of their activities manually and through face-to-face interactions had come to a complete standstill.

The growing need to keep livelihoods going paved the way for the adoption of digital gadgets, catapulting digital payment modes and online transactions. Today, digital payment platforms such as G-pay, Phone-pe and Paytm are available not only at high-end shops but have also been adopted by small businesses such as grocery stores, paan stalls and even auto-rickshaws.

Among the recipients we work with, digital mediums have become a part of everyday life for almost everyone — across farmers, beautypreneurs, street vendors and entrepreneurs with disabilities, the access to smartphones rate stands at 92-100%

In the suburbs of Ahmedabad, REVIVE beauty-preneurs (women running their own beauty enterprises), were also excited to discuss their recently acquired knowledge about digital payment options. Rani, one of our beauty-preneurs, had a particularly interesting story to share: In the excitement of stepping outside her house in the week after a long lockdown, Rani ran to her local supplier and picked up a heavy stock of everything-it-takes to reopen her salon. As she moved towards the cash counter, her enthusiasm waned, as she realised she had left her wallet at home. The next best thing she could do was try remembering her debit card details. No luck. She was relieved when the shopkeeper asked, “Do you have a mobile? Here’s my UPI (United Payments Interface) code.” Rani walked out of the store in amazement at the ease of making payments. “I didn’t even know this was possible, now I ask about UPI everywhere I go,” said Rani.

Additionally, small businesses have started utilising social media as a cheap and targeted means of advertising for their customers in the absence of in-person interactions. In fact, from our own surveys, we found that beauty-preneurs were finding new ways to do business from home during the pandemic. They had started using digital media to spread awareness about their own business and to upskill themselves on current make-up trends.

Asha, one such beauty-prenuer, talked about how she uses Instagram actively to market her parlour to ladies in and around her village. She was amazed at how easily and economically the platform allows her to attract customers by using hashtags and images. For these women, the freedom to market and attract customers on Instagram has given them the kind of outreach that would have been impossible without spending money.

Pradesh in India.

Beyond the livelihood discourse, the availability of banking services over digital platforms has reduced the need to visit banks in real-time and the option to pay bills online has also brought about ease of payments. On the one hand, while these restrictions resulted in unimaginable distress for the socio-economically vulnerable, it also forced them to adopt digital technology to navigate day-to-day activities.

This shift is illustrative of the evolution of digital technologies beyond their conventional use for just communication in Indian society. For example, Uma and Jitubhai from our farmer cohort in Gujarat — post lockdown in 2020 — were hesitant to leave their farm to go to crowded towns for business transactions, for fear of contracting the virus. On a typical day, Uma travelled 100 kilometres to reach the nearest bank to make deposits; Jitubhai would spend an entire day at the electricity office, waiting in line to complete the paperwork for his bills. The pandemic forced them to find new ways to accomplish these tasks and led them to experiment with UPI digital banking, where basic banking services could be conducted at any location, with the tap of a finger. Uma now requests money from sellers for her farm produce through an online payment linked to her bank account and Jitubhai found a way to digitally pay all his bills. For both Uma and Jitubhai, the year forced them to adopt new ways of managing their daily activities and in turn, has resulted in saving time as well as ensuring safety for them and their families by limiting human contact.

In addition to convenience, many beauty-preneurs report that the notion of not having to physically carry around cash provides psychological comfort and safety. Meena, for example, explained that women in her neighbourhood don’t like walking around with cash because they fear they might get robbed. For them, knowing that their cash is accessible in their digital bank account, while not being at risk of theft is a new concept that increases their trust in digital banking.

Many from socio-economically vulnerable communities have displayed astounding resilience in reclaiming their lives and livelihoods during the Covid-19 crisis. However, the adoption of the digital mode has not been uniform in and around the country and there continues to be apprehension towards digital technologies. As the KPMG survey demonstrated, while 8% of the respondents claimed that they were comfortable with exclusively using digital methods of payment, a slightly larger percentage (11%) reported that they would prefer to use cash exclusively over digital modes of payment. The latter statistic is illustrative of the lack of accessibility to digital mediums for all. The overwhelming critique of online education as an exclusive space and the inaccessibility of digital vaccine registration for some, demonstrates that a digital divide still exists in India. Not only is there lack of access to digital gadgets, but also limited access to the internet, which is a necessity for most Indians today.

While accessibility presents a huge issue, lack of trust in digital technologies has also impacted digital attitudes in India. This stems from a lack of knowledge about how digital technologies work and/or from concerns over privacy of one’s personal and financial information. Therefore, we are witnessing a paradoxical case of accelerating digitization with a digital divide that can only be bridged by improving accessibility, transparency and by raising awareness.

It cannot be denied however, that in a lot of ways, the very understanding of technology has catalytically advanced during the pandemic for many Indians — from being a mobile device to an internet portal, to a marketing outlet, to a channel for teaching and banking. It has contributed to efficiency, ease of doing business and the provided the unique opportunity to expand one’s skills for both livelihood and leisure enhancement.

While urgent and pressing issues of financial literacy and digital privacy remain, Leelabai, a member of our farmer cohort, gives us hope about the potential of India’s digital transformation: “Internet penetration will be everything for the women in my village. Especially those who were always constrained by their domestic duties. I can’t wait to see those women have the same freedom and access to the world as their husbands.”